Jonathan Healy | The Industrialization of Embodied Robotic Intelligence

Perspectives

The Industrialization of Embodied Robotic Intelligence

The robotics sector has attracted enormous amounts of capital, some of the best technical talent in the world, and a constant stream of impressive demos that make the future feel just within reach. Yet, outside a relatively small set of controlled environments — industrial automation chief among them — real-world deployments remain thin. Warehouses, farms, factories, hospitals, construction sites: all still look a lot more like the traditional labor landscape than the one promised beneath the billions that have flooded in.

That tension is what makes this moment both compelling and dangerous. For the first time in decades, the hype is underpinned by legitimate structural change: falling component costs, improving battery economics, more capable model architectures, better simulation and training environments, and a talent flywheel powered by capital inflows and AGI-adjacent ambition. The question is not whether the field of robotics shows promise. It’s whether we are at the inflection point of commercial and consumer adoption and how to validate the current momentum.

This piece takes a generalist view of that question. It doesn’t catalog every corner of robotics, from drones to defense to the deepest layers of the autonomy stack. The focus here is broader market context, the forces that have brought us to this moment, and where value most likely accrues.

How Did We Get Here?

Robotics has always held the same underlying premise: turn labor into an automated system. The conceptual roots run deeper than most realize: Egyptian water clocks used automated human figurines as far back as 3000 B.C. However, the term “robot” didn’t enter the modern lexicon until 1920, coined in the Czech play R.U.R. (Rossum’s Universal Robots). In Czech, “robota” translates literally to forced labor or serfdom. The name stuck, and so did the category defining ambition. Strip away the demos, blockbuster funding rounds, and embodied AI discourse, and the underlying proposition remains the same:

Can we build machines that perform economically valuable work in the real world?

A myriad of technological developments have led us to the modern era of robotics. Notably, its important to discuss four distinct eras:

1950 –2000: Industrial Entry & Foundational Build-up

The first era was defined by programmable mechatronics. era, mechanical structure led while compute lagged.

The underlying stack got dramatically more capable in the 1970s. PLCs from Modicon arrived in 1968; the Intel 4004 microprocessor followed in 1971. This was the moment when machine intelligence began to scale economically across industrial automation (Schneider Electric, Intel). By the 1980s (the beginning of the “Digital Factory”), the IBM PC had moved computing into engineering mainstream. Robotics became part of a broader digital production environment — programmed, simulated, monitored, and integrated —rather than an isolated mechanical installation (IBM).

2000 – 2010: Open Robotics & the Mobile Components Era

This is when robotics started to look less like an industrial niche and more like a modern computing field. ROS (Robot Operating System) first commit was made on November 7, 2007 and the PR2 became the canonical research platform, giving the community a shared software layer and common development environment for the first time.

That same year, Apple launched the iPhone. This kicked off the mobile computing and smartphone era and with it, a longstanding cost compression across the supply chain for sensors, batteries, cameras, embedded compute, and power-efficient electronics — all of which robotics would eventually inherit. Universal Robots (founded 2005), iRobot’s Roomba (2002), Kiva Systems (2003) – all were direct beneficiaries. Amazon’s acquisition of Kiva in 2012 was the first real signal that robotics could produce strategic commercial value, not just research excitement.

2010 – 2020: Cobots & Edge Compute

By the mid-2010s, three things converged. (1) Collaborative robots became commercially credible – KUKA LBR iiwa was the first series-produced sensitive robot certified for human-robot collaboration, while Universal Robots kept pushing on accessibility and ease of deployment. (2) GPU compute became practical at the edge – Nvidia Jetson’s launch in 2014 brought real-time AI and computer vision closer to deployable systems (building off CUDA in 2006 and later transformer architecture). (3) The AI stack shifted in a fundamental way– breakthroughs in policy optimization (Trust Region Policy Optimization), fast adaptation (Model-Agnostic Meta-Learning), and richer perception architectures (Non-Local Neural Networks) began replacing hand-engineered pipelines with end-to-end, data-driven perception and control.

The net result was robots moving from structured, hard-coded rules toward perception-based learning through reinforcement learning, simulation, and imitation — acquiring motor skills from data rather than from explicit hard-coded programming. This set the critical foundation for what was to come next.

2020 – Today: Physical AI

Over the past decade, Google’s infamous 2017 transformer paper translated to RT-1 (2022), which framed robot control as a transformer problem trained on large, diverse real-world datasets. Next came RT-2 (2023), expanding into a vision-language-action (VLA) model that learned from both web and robotics data. NVIDIA announced Project GR00T in 2024 and in 2025 GR00T N1, an open humanoid robot foundation model. The robot “brain” was beginning to take shape, alongside new age robotic model labs (e.g., Physical Intelligence, Skild AI, Field AI).

Notably, other underlying infrastructure improved in parallel. For example, 5G enabled faster wireless connectivity and more reliable teleoperation while better data pipelines and more capable hardware in the field opened the door to broader remote operations, fleet software, and data collection loops. In short, many threads were converging at once.

The Enabling Economics.

With every meaningful market shift, it’s worth diving into the enabling paradigms. In robotics, two cost curves matter most: (1) components and system cost and (2) human labor cost. It’s the delta between the two that make robotics attractive today from a purely economic standpoint, though many other factors like labor availability, political pressure and societal acceptance are also at play.

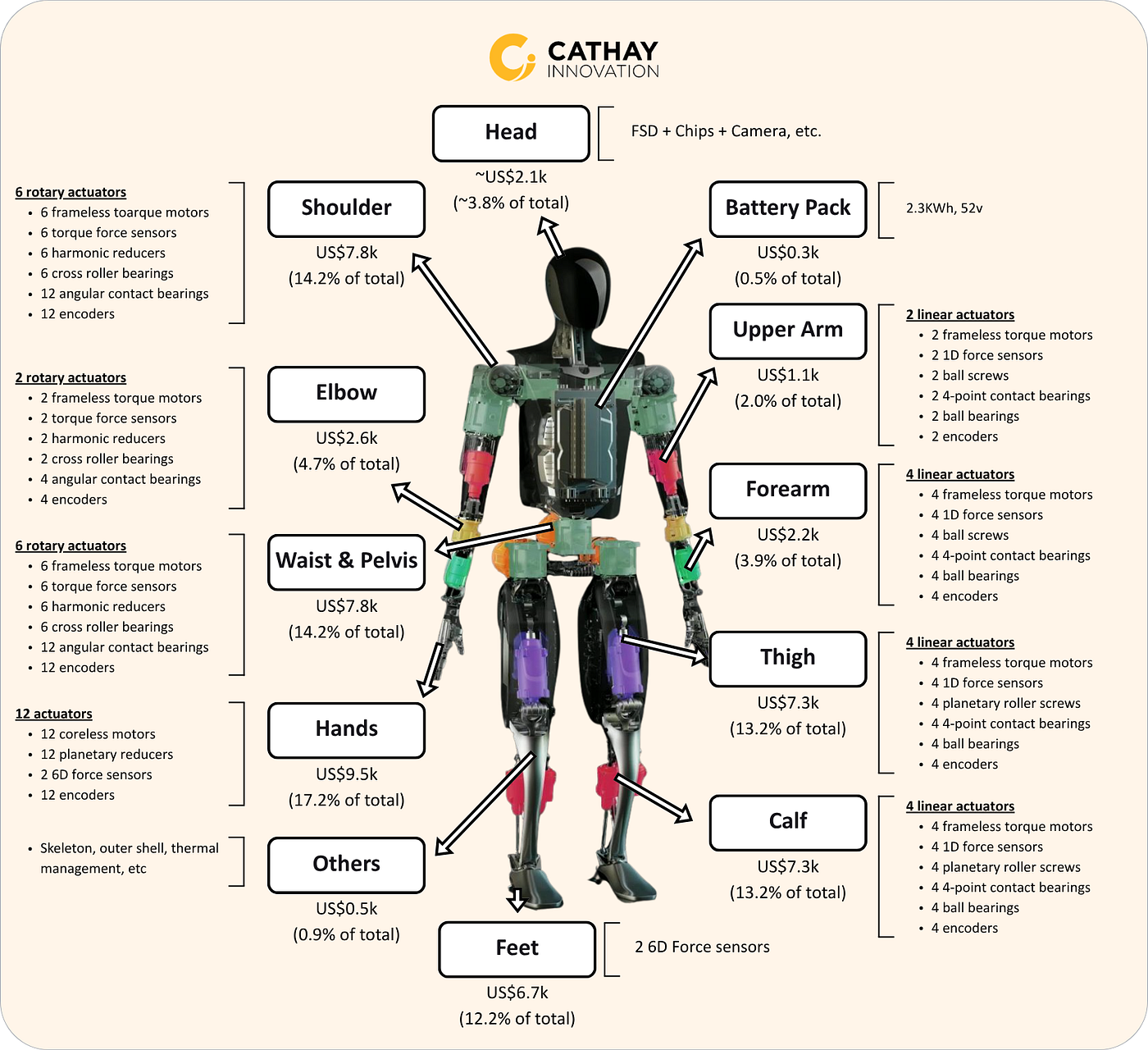

On the system side, key components typically include actuators, sensors, batteries, semiconductors / chips, and mechanical structures. Humanoids include most of these, so they serve as a reasonable proxy even if they’re not representative of all robotic systems. Luckily, Morgan Stanley previously broke down Tesla’s Optimus BOM by section which illustrated the contribution of each within the full system (see Figure 1 below).

Figure 1. Optimus Humanoid BOM breakdown (from Morgan Stanley Feb 2025 estimates)

However, a full cost breakdown alone misses the underlying economic shifts enabling the next wave of robotics. Thus, it’s important to discuss a few specific cost curves:

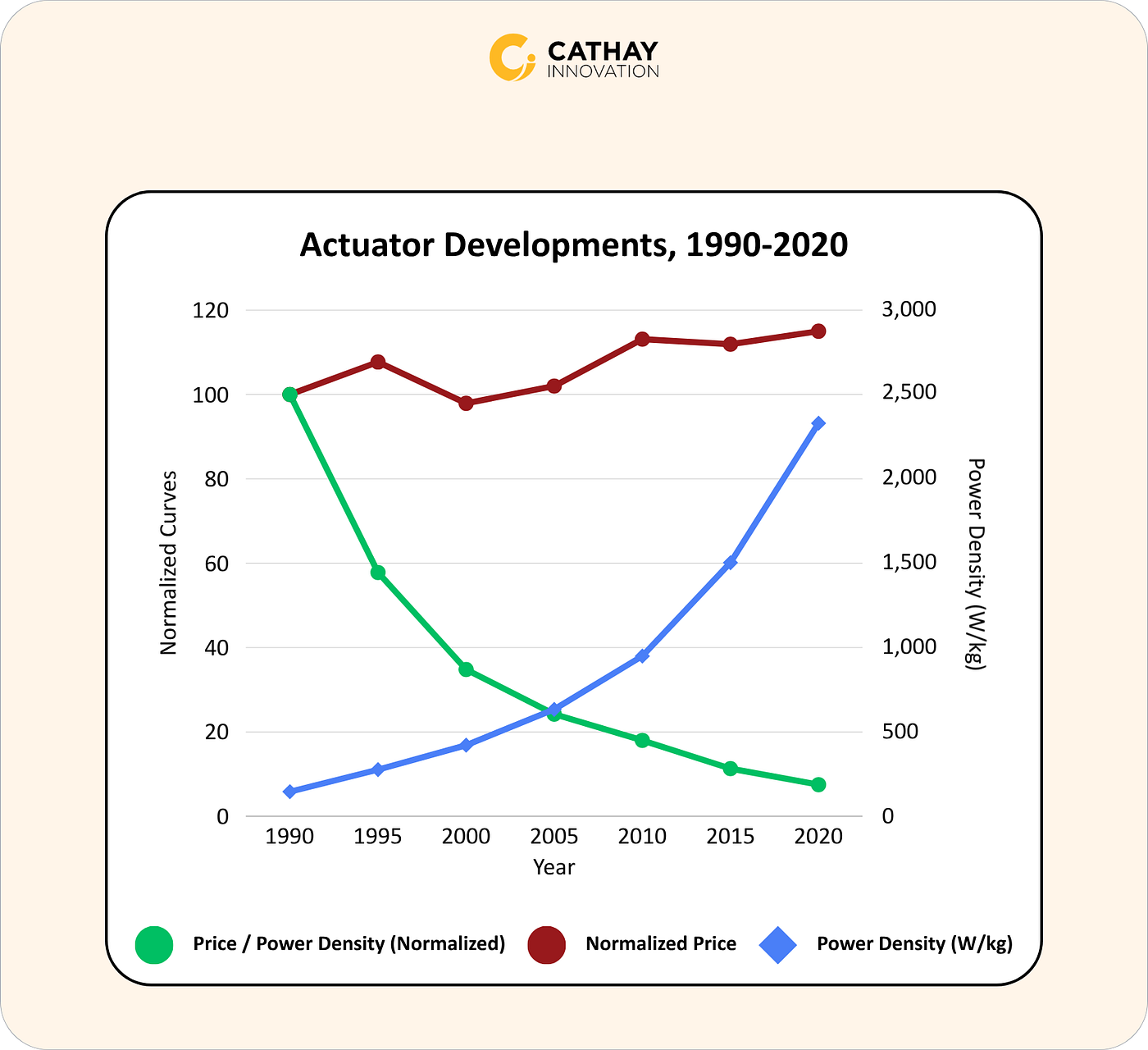

1. Actuators – represent the plurality of cost in many robotic systems.

China dominates the market which complicates certain use-cases and supply chain resilience. As seen in Figure 2 below, while the headline price trend is not flattering with average actuator prices growing above inflation (per FRED), the actual outlook improves meaningfully when normalized for density (per Sayako and Akiya). Yet, this still misses the quality adjustment: electric linear actuators have continued to improve in precision, control and refined motion, with research on permanent-magnet linear motors showing tracking error fall from under 7 μm in 2003 to roughly 0.5 μm RMS in later work (

Figure 2. Plot of actuator price as a function of power density (for electric actuators)

2. Battery Costs – have fallen precipitously, driven by the automotive industry and grid level storage.

Using one of the most common formulations, Li-Ion, we can see in Figure 3 that costs per kWh since 2013 have dropped a whopping ~87% and even since 2020 realized a ~36% decrease with a plateau in sight.

Figure 3. Bloomberg NEF 2025 Li-ion battery price survey

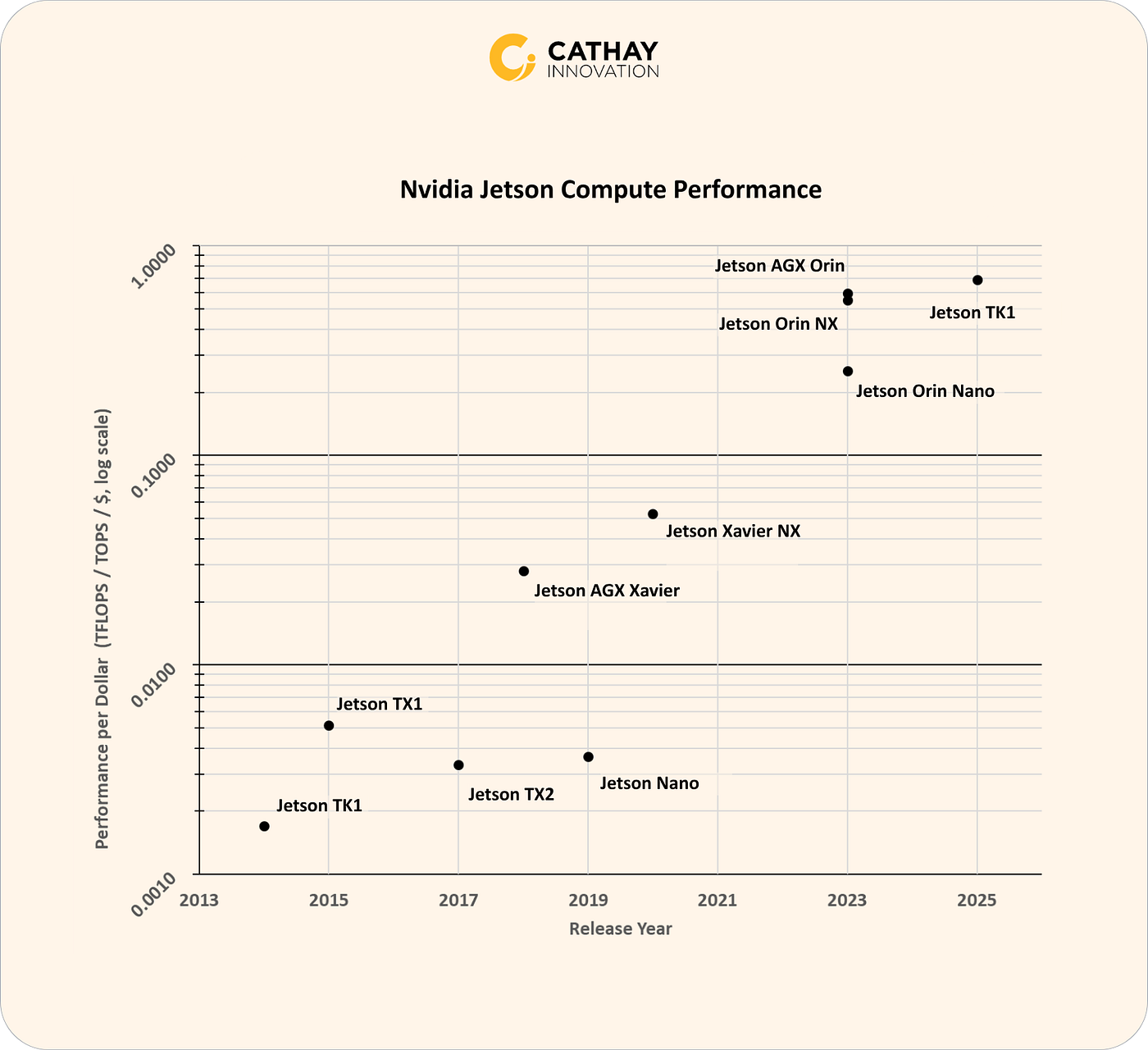

3. Compute Cost – is not a direct BOM line item, but it’s central to the long-term economics.

The case for robotics outcompeting labor depends in part on the continuing decline in edge compute cost and the improving performance of parametrized models. Using Nvidia’s Jetson series chip as an example (see Figure 4), it becomes abundantly clear the order of magnitude improvement in performance per dollar since 2014.

Figure 4. Value of Nvidia Jetson chip performance over time (based on initial performance and price

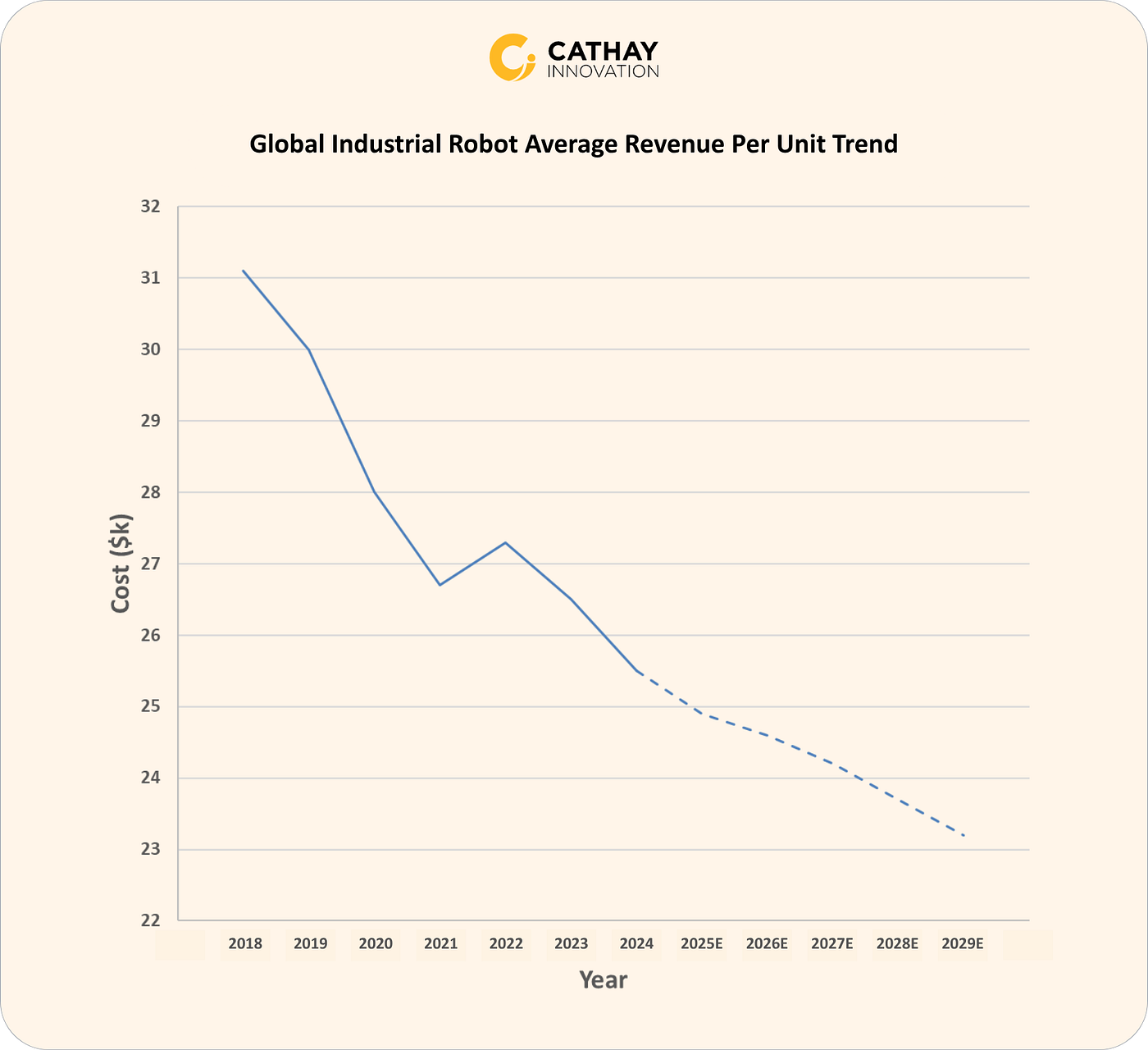

4. System Costs – taken in totality, using industrial robots as an example, has fallen substantially over the past three decades with further declines projected (as shown in Figure 5).

Figure 5. Industrial robot cost since 1995 (Interact Analysis)

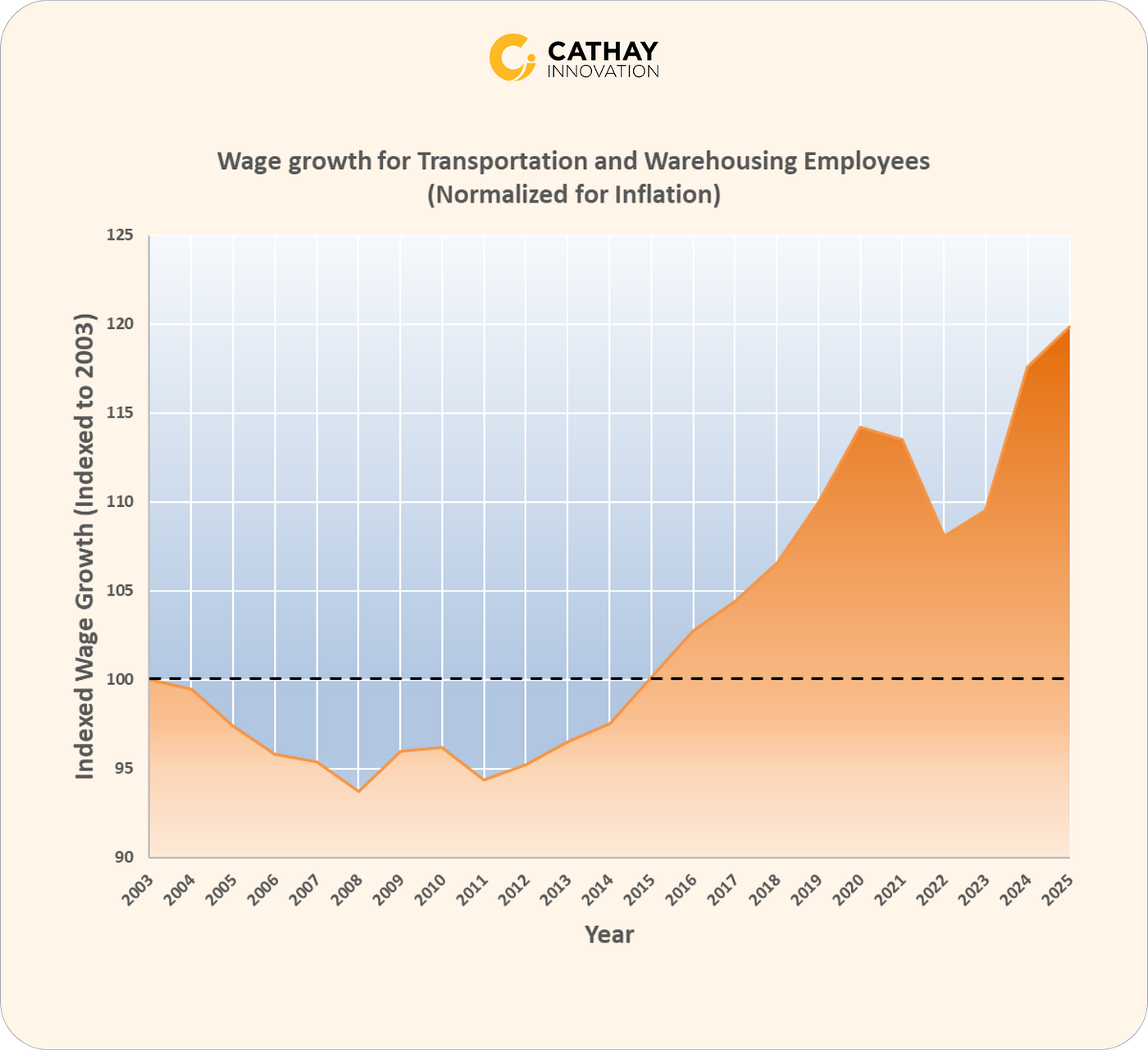

5. Labor Cost in the US – looking at warehousing and logistics (a typical use-case), we’re seeing a move in the opposite direction with average hourly wages rising steadily.

For example, Figure 6 shows the wage growth for transportation and warehouse employees indexed to 2003 (per FRED). Even when normalizing for inflation there has been an outpacing of wage growth underpinning the critical nature of labor demand in this sector.

Figure 6. Annual wage growth of Private industry workers in Transportation and warehousing (per FRED)

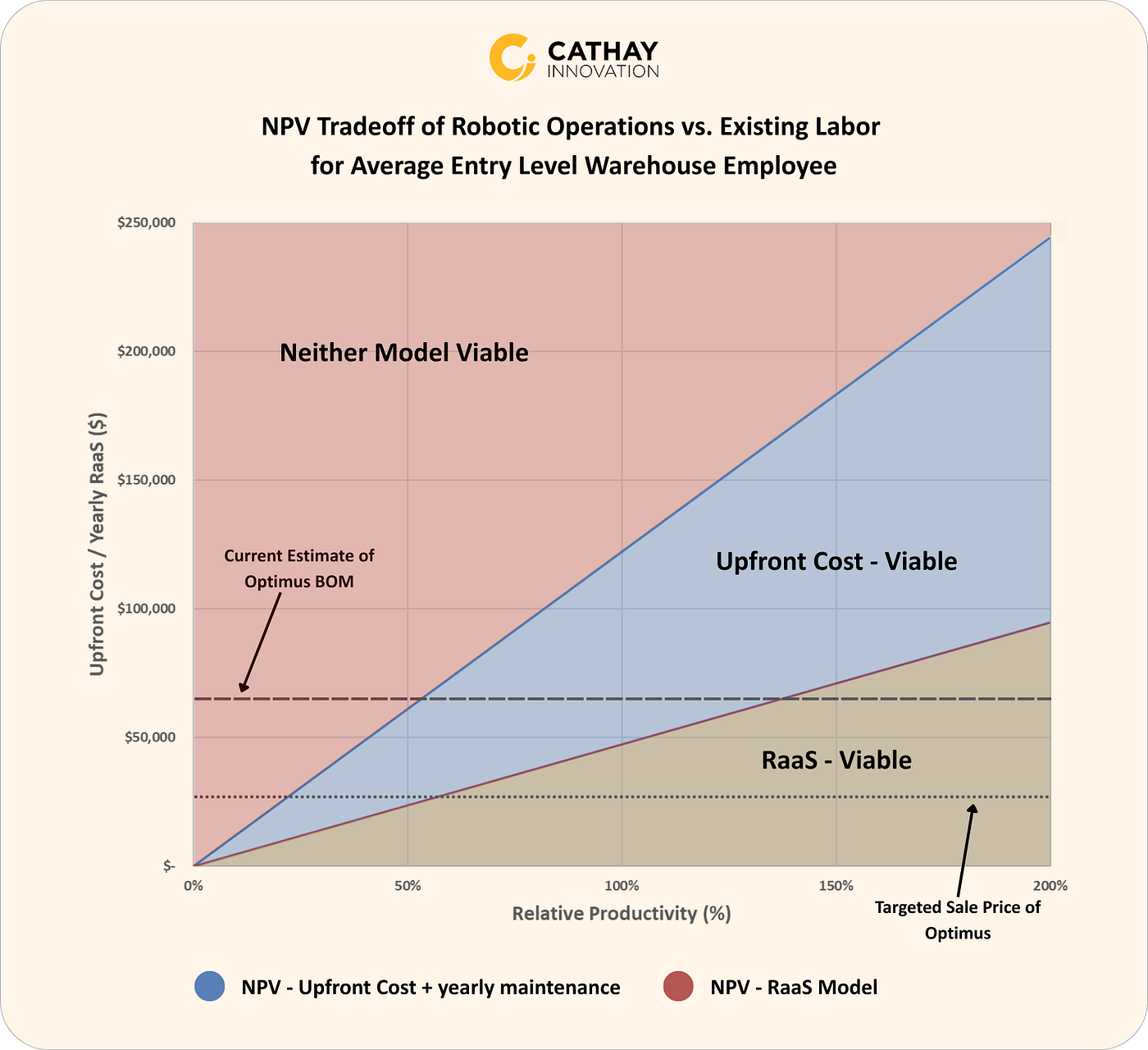

Put those curves together and the conclusion is relatively clear: the marginal value of automation / robotics is increasing. Plotting this on a NPV basis illustrates this clearly (see Figure 7 below) though depending on the model, the “efficient frontier” will vary.

Figure 7. Efficient frontier of robotics deployments for an entry-level warehouse operations use-case. Assumptions include: average entry-level warehouse wages and benefits from Indeed, useful lifetime of 8 years, 20% ongoing maintenance cost in upfront model, 10% discount rate.

The market tailwinds certainly support the case for a clear market need and demand. Yet, the fundamental question remains:

Are we at the inflection point for robotic adoption?

A few distinct tradeoffs are still playing out (at both the regional and company level), each worth naming briefly:

–> Hardware vs. Intelligence – largely the story of different approaches from China to the US in the most recent wave. Existing manufacturing infrastructure and installed supply chains favored hardware development in China; while the US had a head start in AI/ML and early LLM foundational model labs. Though, expect more crossover over time.

–> Industrial vs. Consumer – picking and packing pallets may look superficially similar to picking up dishes though the motion, grip dynamics, and pressure tolerances are not. Given the already strong presence of robotics in industrial settings and the clear ROI, deployment will scale here before humanoids mass-populate the home.

–> Open-sourced (Android) vs. Closed (iOS) – much like the Android/iOS split in smartphones, robotics is beginning to divide between open, developer-centric platforms (e.g., ROS equivalents, open hardware ecosystems) and vertically integrated, closed systems where hardware, software, and models are tightly controlled.

Beyond Econ: The Intelligence Stack.

Falling component costs explain why robotics is more financeable than it was even a few years ago. However, they do not explain why the market’s narrative shifted from narrow automation to general-purpose robotics. That shift is about the intelligence layer.

Robots are moving from more simplistic engineered perception, planning, and world assumptions toward learned representations trained on large-scale video, robot demonstrations, synthetic projections, and multimodal inputs. Three areas worth considering:

-

The Data Problem

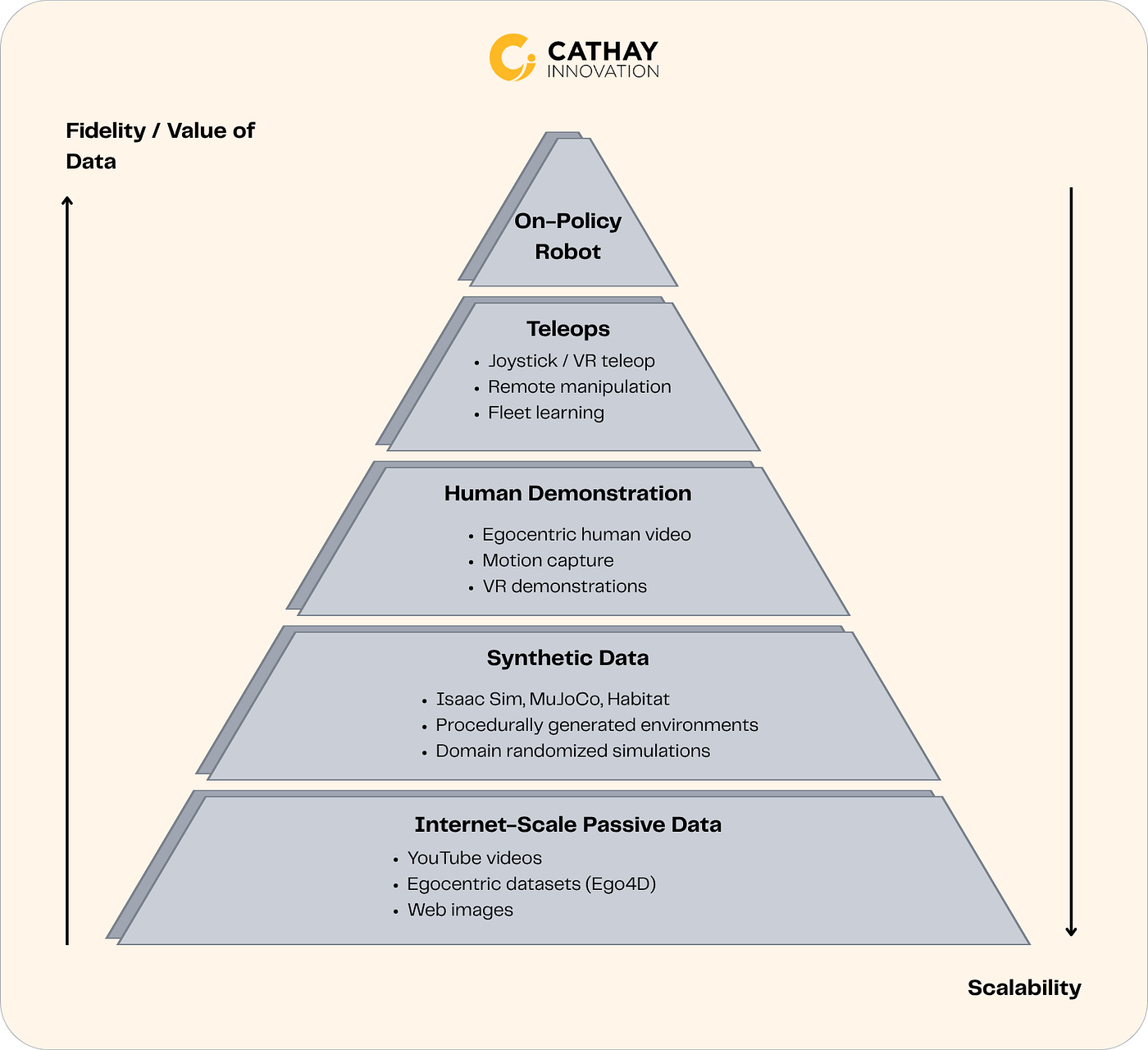

The implication is simple: robotics still lacks its physical equivalent of the Internet. LLMs harvested digitized text and media while robot learning still depends on teleoperation and human operators, physical hardware, and real-world environments (robots occasionally drop their coffee too!). The gap is vivid: roughly ~1B hours of internet video to 350M hours of autonomous-driving data to ~20M hours in a world-model training proxy (like Cosmos), and only 300K hours of robot-manipulation data globally (per Bessemer’s recent report). Even granting the imperfect comparisons across modalities, robotic intelligence is fundamentally data constrained. Further, not all data is created equal nor usable and this is generally inversely correlated to scalability of the data. Figure 8 below highlights some of the main categories worth considering.

Figure 8. Robotic data layering – Value vs. Scalability

-

The Intelligence Layer is Becoming Performant

Both world knowledge (world models) and action knowledge (Vision-Language-Model / Vision-Language-Action model, multi-modal robotic foundational models) have advanced quickly. World knowledge —how objects behave, liquids pour, fabrics drape — can increasingly be learned from abundant video and modeling (see here). Action knowledge — how a specific arm, hand, or humanoid translates commands into motion — remains embodiment-specific, but may require far less robot-specific data than prior generations assumed.

was pretrained on over one million hours of video, then action-conditioned with less than 62 hours of robot footage. Google’s RT-2 extended web-scale vision-language learning into actual robotic control. Simulators are not dead, locomotion still maps well to formal physics engines, but their role is narrowing. Contact-rich manipulation is where learned world models start to matter more.

-

Translating Theory into Solutions

First, they came for the data, then they built the models, and then what was left? The actual solution (the important stuff!): moving pallets, caring for patients, welding sheet metal. Better models show up first as practical gains: better grasping, fewer teleop interventions, faster adaptation to new SKUs, more robust manipulation, longer autonomy windows inside bounded workflows. While the “ChatGPT moment” debate for robotics continues, the more relevant question is whether this new intelligence layer is good enough to push more physical tasks over the threshold from pilot to production.

The stack resolves from there. Data enablement builds the corpus. Robotic neo labs turn that corpus into reusable intelligence. Vertical solution providers turn that intelligence into measurable labor economics.

Where We’re Looking.

The robotics landscape today is as broad as it is messy hence intentionally avoiding commentary on all aspects, especially standalone markets (e.g., drones, defense, the deeper autonomy, and large swaths of factory automation). Our interest sits at the intersection of the three core bottlenecks described below:

-

Dearth of Data Availability -> Data Enablement

If robotics is fundamentally data-constrained, then data enablement is one of the most important near-term categories in the stack. The market still lacks a scaled library of physical-world data, and someone has to build both the picks and shovels and the underlying commodity. This includes capturing egocentric and teleop data, generating synthetic environments, evaluating edge cases, cleaning signals, and creating the feedback loops that let systems improve over time. The opportunity here is real and immediate. But it’s also already crowded. The reference points to watch are Scale AI (data labeling and annotation) and Mercor / Mirco1 (human data) to show what can be unlocked at scale. Much like the early data-labeling wave in AI, the strongest businesses will likely use an initial service or tooling wedge to move into higher-value workflow software, model-adjacent tooling, or proprietary data loops that are hard to displace. This time around, it might even involve a hint of hardware.

-

Still Nascent Intelligence Layer -> Robotic Neo Labs

If the intelligence layer is becoming more useful but still early, then robotics neo labs are the next logical area. These are the companies trying to turn once fragmented physical-world models into reusable intelligence. Value will accrue to teams building around world models, action models, multimodal robotic foundation models, and the tooling to train, evaluate, and deploy them. Much of this cycle’s excitement has already flowed here: Skild, Physical Intelligence and Field AI (among many others) are all at multi-billion valuations, beginning the robotic lab king making cycle. But our interest is more on what gets built around and beneath the lab itself. . The labs may capture the narrative, but the real winners will be those that turn it into a product that addresses real-world problems at commercial scale.

Exit pathways here will also look different than prior robotics cycles. If the current pace of excitement holds, traditional milestones may matter less than speed, talent density, proprietary data, and technical position, especially for pre-commercialized labs and infrastructure players. Expect more acquihires, IP-driven outcomes, and strategic partnerships than the classic robotics playbook. It wouldn’t be surprising to see renewed focus on edge inference and specialized on-device compute as labs and partners look to reduce dependence on high-cost centralized compute.

-

Translating Technical Progress into Real Workflow Outcomes -> Vertical Solution Providers (VSPs)

If better intelligence is finally making robots more capable inside bounded environments, the most immediate commercial beneficiaries are the companies deploying it into real customer workflows. This is where technical progress meets economic reality in the VSPs. Many physical workflows are constrained enough to be learnable, valuable enough to justify deployment, and messy enough that better intelligence was the missing piece.

The difficulty here is the lack of universal adoption standards. Customers evaluate on a sliding scale between speed (e.g., items packed / hour), accuracy (e.g., items correctly picked / all items packed), and cost (e.g., levelized hourly cost), with labor efficiency as the ultimate metric. Expect scale-up to start as workforce augmentation, finding particular ROI in understaffed segments and periods of low labor availability (e.g., night shifts, weekends) where lower speed and accuracy thresholds can justify higher initial costs while domestic scale accumulates.

The next enablement layer is already starting to come into view as the bottleneck shifts to adoption at scale: integration, servicing, uptime management, maintenance, and financing. Formic was early in pointing to this reality, but the broader lesson is straightforward: as robotics moves from pilots to fleets, the surrounding ecosystem becomes investable too. In many markets, that’s where durable companies ultimately get built.

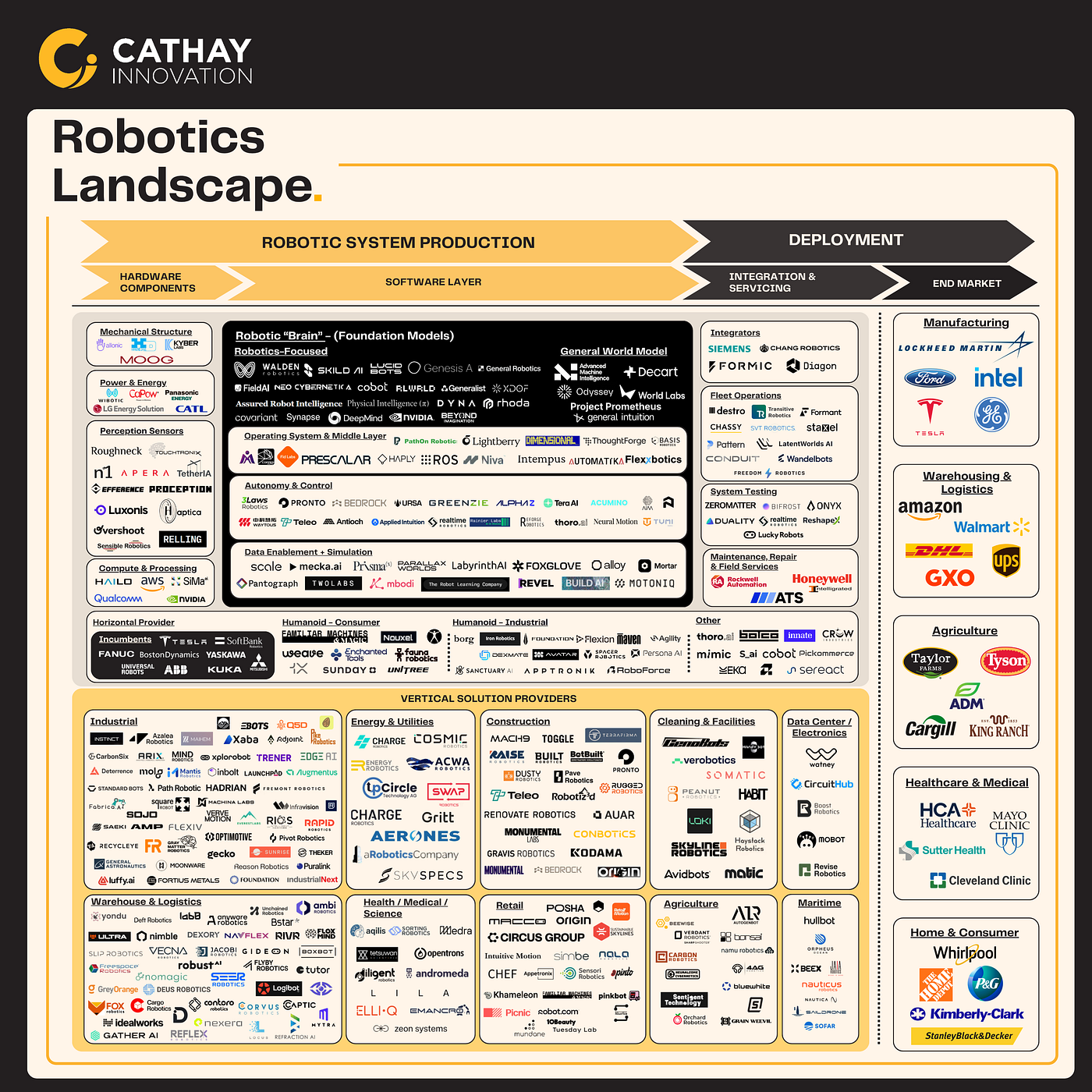

Below is a mapping of these categories and where they sit in the broader robotics value chain. It is a simplified view — many companies straddle multiple areas — but useful for conveying the scale and flow of of the sector.

Figure 9. Cathay Innovation Robotics Landscape Market Map

How Can You Help?

Most of the above draws on primary research, deal experience, and widely cited third-party data — but the most valuable signal right now is ground-level. What are operators actually seeing? Which deployments are hitting production? Where are the pilots stalling?

If you’re building in this space – give us a holler.

Words by Jonathan Healy ; Edits by Jaclyn Hartnett

NEWS