Jonathan Healy | Redefining the Mining Value Chain

Perspectives

Written by Jonathan Healy, Investor, San Francisco

The State of Mining Affairs.

Once dismissed by capital markets as slow, capital intensive and a technology laggard, the mining sector is quietly reemerging as a strategic pillar of the global economy. While the full impact is still unfolding, signs of large-scale intervention are increasingly visible across both public and private sectors. Take for example the hotly debated decision for the U.S. government to acquire an equity stake in MP Materials to secure domestic rare earths, GM striking direct supply agreements with Thacker Pass, along with a wave of critical mineral legislation worldwide.

This shift is not only top-down. New entrants such as KoBold Metals — founded in 2018, now valued at over $4B, and working with the U.S. State Department to secure mining rights in the Congo — highlights the speed at which disruption can happen, even from the company-formation level. What appeared as isolated headlines, now form a clear pattern: a Western mining industry entering a period of structural transition and rapid expansion.

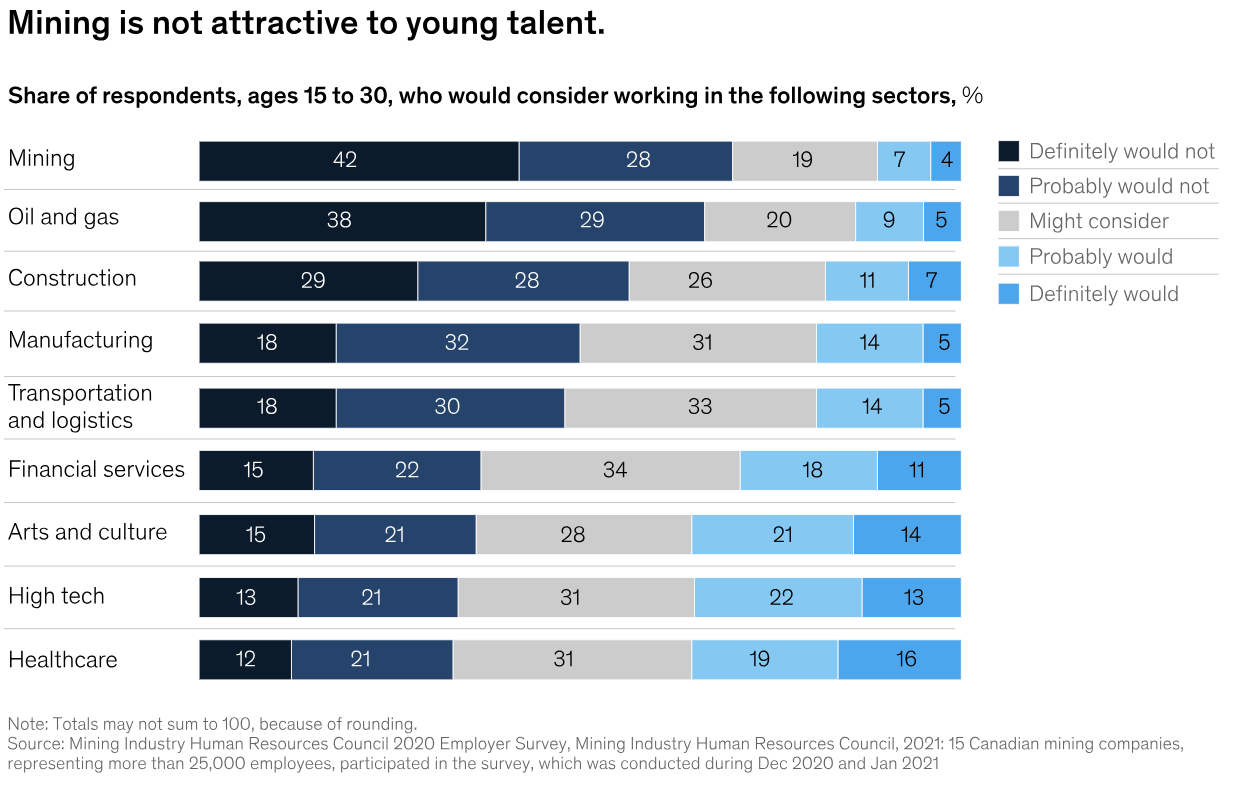

Behind these moves sits a broader shift: mineral supply chains are becoming matters of national security, the energy transition is driving up demand, and now the sector must contend with the impact of AI while managing perception challenges with the next generation workforce (see Figure 1).

To put it in practical terms, just to meet battery needs in 2030 would require $285B in investment and the addition of 293 average-sized mines, more than the 2023 total amount of active US metals mines (Benchmark, CDC). Adding to the dilemma is the fact that our current mines are running out, and new resource discoveries are down as much as ~80% since the 1990’s (S&P). One step down, China’s dominance across mining, refining, and manufacturing has pushed Western economies toward “mine-to-market localization.” On the heels of this alarming backdrop, “the age of AI” has practically translated to higher-order compute, multimodal modeling, and geospatial foundation models enabling miners to find new deposits, evaluate assets, and accelerate development. AI needs minerals; minerals need AI. The two markets are colliding — the result is a wave of renewed investor attention across the mining value chain.

Market Dynamics — Why Now is the Time for Disruption.

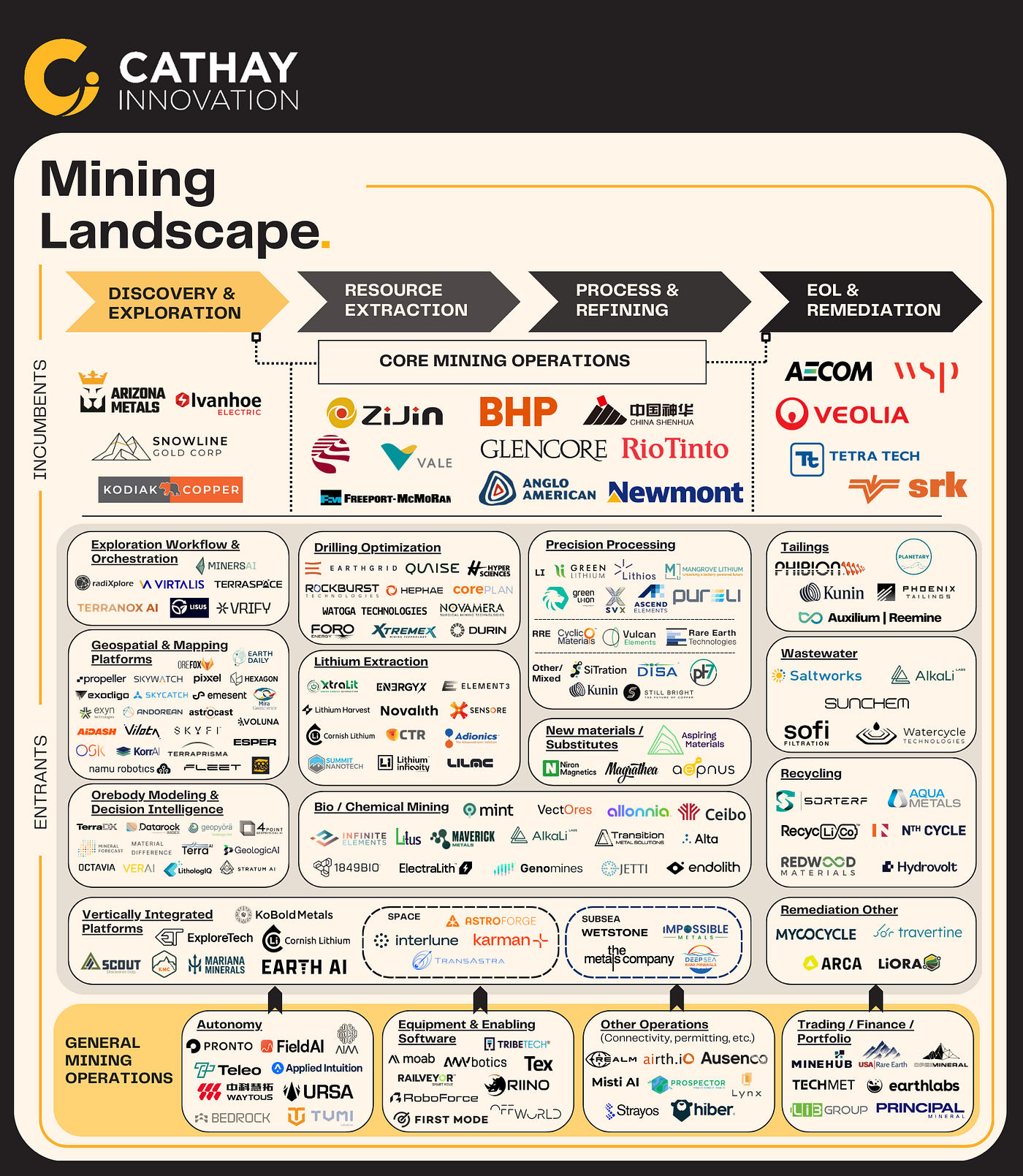

Mining remains one of the most complex and risk-laden industrial value chains, with each stage introducing its own uncertainties — from discovery (greenfields) and definitional exploration (resource definition / advanced exploration), through feasibility (PFS / BFS), development and construction, and mine operations, to processing and refining, offtake and trading, and ultimately reclamation and closure. Below is a truncated version of this value chain, noting where early-stage entrants and established incumbents are currently positioned (see Figure 2).

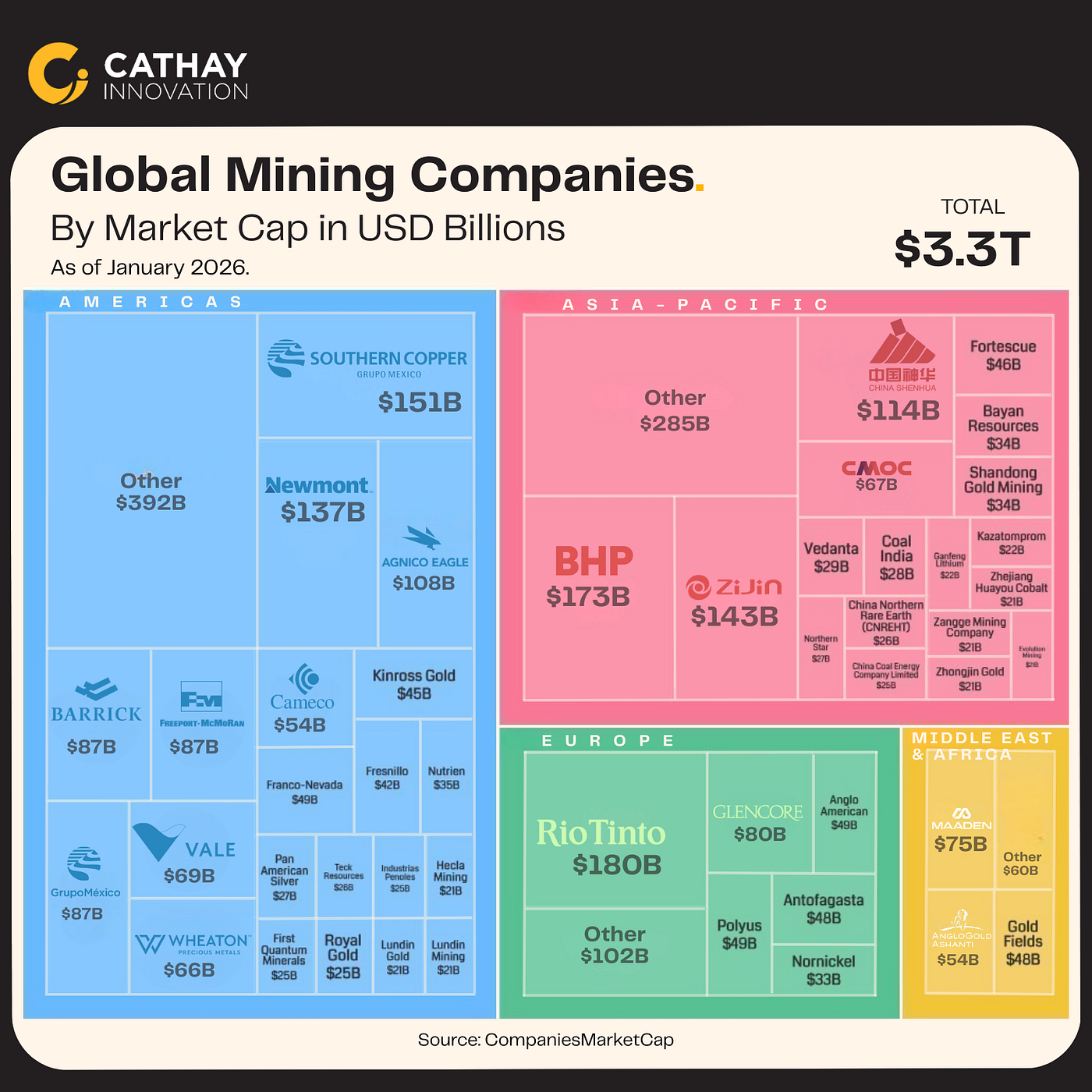

This lifecycle is managed by roughly 3 classifications of players. At the leading edge, are the ~11,000 micro-sized junior explorers (assets sub $1b)1 managing only a handful of early-stage projects but representing ~70% of discoveries. Smaller assets, once characterized and de-risked, move to mid-tier miners (~300). At the top sit global majors like BHP, Rio Tinto, Glencore, Freeport-McMoRan, and China’s Zijin, each managing hundreds of large assets across continents (see Figure 3). The market cap distribution reflects this asymmetry: the top 10 mining companies dominate a ~$1T aggregate market, with everyone below the majors fighting for relevance, capital, and offtake agreements. This concentration creates structural inertia but also exposes points where technology can unlock outsized leverage.

At the same time, macro demand signals are accelerating faster than the industry can respond. Energy-transition metals like lithium, copper, nickel, and rare earths are now explicitly framed as strategic assets, with COVID-era supply shocks and China’s dominance in refining and processing reframing the sector through a national-security lens. Electrification requires orders-of-magnitude more mined inputs, with analysts projecting copper demand growing 24% by 2035 (Wood Mackenzie), and similar trends across other battery metals. Beyond the green economy, sectors like automotive, aerospace/defense, and hyperscale datacenter buildout are intensifying demand, placing further pressure on an already constrained system. For example, each 1GW datacenter requires 27,000 tons of Copper, equivalent to 2.5% of America’s output2 which, according to BHP, will grow 6x by 2050 (from 0.5m tons today). Yet, supply continues to lag: permitting timelines of 10–15+ years in western jurisdictions routinely push projects beyond economic viability, creating a structural gap between the world’s material demand and the production capacity needed to meet it.

These pressures are reshaping investor behavior. Venture investment in mining innovation has grown >10x since 2020 (CleanTech Group), but remains concentrated in early-stage prospecting tools, leaving the “missing middle” of feasibility, modeling, processing, and development vastly underserved despite being the most value-determinative. Meanwhile, AI has become the industry’s great unlock through advances in multimodal geoscience models, higher-order compute, cloud-native simulation, and real-time sensing that can integrate datasets previously trapped in silos and meaningfully improve decisions across discovery, exploration, feasibility, and operations. Parallel to this, global OEMs (e.g., Tesla, GM) are pursuing closer integration into upstream supply, though these moves bring tradeoffs: low-margin, high-capex segments only make sense if technology compresses schedules, improves yield, or de-risks capital commitments.

There remains an open question of whether the market already prices in this reality. Traditional miners trade at mid single-digit to low teens EV/EBITDA multiples (e.g., BHP at ~7 while Glencore sits at ~15) 3 with limited growth strategies beyond acquisition. Meanwhile, copper, gold, and silver are at all-time highs and royalty and streaming companies like Wheaton Precious Metals and Franco Nevada trade around 30–35×3. This gap reflects operational and geologic risk discounting embedded in mining. Technology that shortens development time and reduces risk anywhere in the value chain effectively moves enterprises from a “mining multiple” to a “growth industrial multiple” — and that is where venture-scale opportunity emerges.

Market Opportunity & Evaluation Framework.

Mining’s structural bottlenecks are well known, but they have intensified to the point where they now define the investable landscape. The largest failure sits in the post-discovery exploration-to-development gap, where capital needs increase to tens of millions, false positives remain high, and timelines are still a decade or more away. Data is scattered across geoscience domains, assay labs introduce multi-month lag, and geologic models rely on human assumptions rather than probabilistic models. As a result, mine lead times have stretched to ~18 years for recent projects, up from ~13 years a decade and a half ago. Nearly 40% of delays stem from permitting, and 80%+ of major developments blow past cost or schedule targets largely due to poor front-end risk qualification (sources: McKinsey & Company, Norton Rose Fulbright, EY). These delays are not merely operational headaches but existential when you consider that a $3–5B project loses ~$20M in NPV per week when production slips (ERM).

These breakpoints create clear whitespace. On the front end, anything that compresses the drill -> data -> interpretation -> retargeting loop directly attacks the longest critical path in development. Faster assays, automated geologic and geophysical data fusion, probabilistic resource modeling, and scenario optimization all reduce uncertainty at the point where uncertainty is highest and capital need is spiking.

Adjacent to this, permitting and social-license tooling — like workflow orchestration, traceability, impact modeling or community analytics — targets the regulatory choke points validated by SME and ERM studies. Further downstream, opportunities appear in refining resilience (process intensification, DLE, recycling), tailings monitoring and governance, and workforce-leverage systems like AI copilots and remote-ops tooling. Not all processing innovations translate cleanly into venture-scale value given the concentrated midstream, so investors must be selective.

Stepping back, these dynamics point to new types of mining companies. In one version, they partner with juniors, provide software and modeling services, and captures upside through equity-style exposure rather than owning high-capex assets. Because royalty businesses trade at structurally higher multiples than operators, technologies that quantify uncertainty or compress timelines can effectively underwrite a new asset class at the intersection of mining tech and fintech. An alternative higher capital intensity approach, includes those looking at streamlining development and mining pathways by verticalizing operations, usually on a smaller scale or stranded asset passed by majors. On these assets, even 5–10% improvements in processing or operating efficiency have reflexive, multiplicative impacts on margins, free cash flow, and ultimately equity value, enabling upside rather than pure operating cost benefits.

To evaluate these opportunities, we apply a Capital Intensity vs. Time-to-Value lens — complemented by criteria such as:

–> Cycle-time compression on a known bottleneck

–> Risk delta (schedule, capex, ESG, midstream exposure)

–> Switching cost & data flywheel

–> Capital intensity & gross margin structure

–> Time-to-first-value, ideally measured in weeks/quarters

Taken together, these criteria help distinguish not only promising technologies but venture-backable companies — those capable of capturing value in a sector where value has historically been consumed by risk, delay, and capital inefficiency.

Our Areas of Interest.

As the industry confronts structural bottlenecks in discovery, feasibility, and processing, we see a set of emerging technologies that are not only technically promising but also aligned with venture-style value capture. Two themes stand out where Cathay Innovation has built conviction: decision intelligence for exploration and next-generation sensing for both primary and secondary supply.

Discovery & Exploration — AI-Enabled Decision Systems + New Business Models

The wedge? AI Decisioning Platforms

AI-driven decision platforms that compress the drill → data → interpretation → retargeting cycle. By shifting exploration from intuition-driven workflows to probabilistic, repeatable modeling, these systems raise discovery rates while shaving years off development timelines.

Why now? Compute and Demand

Advances in generative modeling, probabilistic simulation, and domain-specific geologic encompassed data architectures are arriving just as global supply chains urgently need new critical material deposits. Technical maturity and market demand are aligning simultaneously for the first time.

What’s missing? Business-model innovation

Most exploration tech today sells software or services and captures little of the upside it creates. The next generation will need mechanisms like royalties, contingent equity, or derivative exposure, transforming these platforms from “tools” into scalable financial exposure vehicles — more akin to Franco-Nevada than a contract geoscience firm.

Enhanced Data Capture — Unique Sensors for Mining & Beyond

The wedge? New sensor modalities

Technologies such as muon tomography (Ideon) or neutron-based prospecting (Voluna) allow explorers and operators to “see through rock” in ways previously impossible.

Why now? Cost and sustainability paradigm

Exploration is capital constrained while ESG pressure remains high in global markets. Sensors that deliver higher-confidence resource estimates or unlock new supply from secondary sources directly address cost and sustainability pain points.

What’s Missing? Defensible business models

Most sensing companies remain stuck in hardware-plus-services models. The opportunity is in pairing sensors with automated interpretation and decision systems. This turns raw data into actionable models and builds recurring revenue with defensible data moats, rather than one-off hardware sales.

Closing Thoughts.

The mining sector is entering a pivotal decade: long timelines, concentrated incumbents, and systemic chokepoints have turned critical minerals into matters of national strategy, not just industrial supply. As exploration and feasibility become the binding constraints on global material demand, the industry is shifting from human-driven geology to data-driven decision systems. Mining is becoming a data industry disguised as a materials industry.

For Cathay Innovation, the generational opportunity lies where new business models intersect with the highest-leverage stages of the value chain, transforming geological uncertainty into investable, repeatable, and scalable products. With strategic partners like Vale and COPEC (via WIND Ventures), we’re positioned to help the next wave of mining innovators navigate both the industrial and commercial pathways. If you’re building in these spaces, let’s talk.

Special thanks to Danny Donahue (Terra AI), Ted Feldman (Durin), Daniel Rau (Kunin), and Elliot Forcier-Poirer (Watoga Technologies) for their input and feedback on shaping this work.

About the Author

Jon is a Vice President at Cathay Innovation in San Francisco. He focuses on startups at the intersection of physical and digital industries, with a particular interest in AI applications in manufacturing, supply chain, energy, and mobility. Since joining in 2023, he has been instrumental in sourcing and leading investments including David Energy and GenLogs, partnering closely with both founding teams as they scale.

Before Cathay Innovation, Jon was a Business Analyst at McKinsey, focusing on Private Equity and Aerospace & Defense, and a Venture Analyst at FedTech, a deep tech venture builder. He began his career as a Materials Engineer at the U.S. Department of Defense’s Naval Surface Warfare Center.

Jon holds a B.S. in Materials Science and Engineering and an M.S. in Finance from Case Western Reserve University. Outside of work, he is an avid Buffalo Bills fan, enjoys skiing, and often leads the charge on the soccer field in his Sunday league matches.

NEWS